Personal trainers typically need public liability insurance and professional indemnity insurance as a minimum, with additional cover depending on how and where they work.

This guide explains what personal training insurance you need as a PT, how much it costs, whether online coaches need cover, and how to choose the best policy.

Content:

- Do You Need Insurance To Be a Personal Trainer?

- What Insurance Do Personal Trainers Need?

- What Does Personal Trainer Insurance Cover?

- Do You Need Insurance As An Online Personal Trainer?

- Do you Need Insurance If You Work in a Gym?

- Do You Need Insurance to Teach Group Fitness Classes?

- Do You Need Personal Trainer Insurance to Work Abroad?

- Do Personal Trainers Need Employer’s Liability Insurance?

- How Much Is Insurance For a PT?

- How to Choose The Best Personal Training Insurance

- Personal Trainer Insurance FAQs

Do You Need Insurance To Be A Personal Trainer?

Yes, personal trainers should have insurance in place regardless of whether they work in a gym, freelance, run classes, or coach online.

Being insured is important as it covers you should you practice outside the legal limitations of a personal trainer.

While you want to make money as a personal trainer with plenty of clients, having personal trainer insurance will give you financial protection if this does occur.

What Insurance Do Personal Trainers Need?

All personal trainers should have core cover in place, with additional insurance depending on how and where they operate.

Legally Required Personal Trainer Insurance:

There are 2 types of personal trainer insurance which are legally required for you to work as one.

#1 – Personal Trainer Public Liability Insurance

The most important type of personal trainer insurance is public liability insurance, this may also be referred to as ‘personal trainer liability insurance’ or ‘professional liability insurance for personal trainers’.

This is the minimum legal requirement needed to operate as a personal trainer, which covers:

- Injury to a client under your supervision

- Damage to equipment owned by the gym you are operating in

- Equipment failure resulting in injury to the client

For example, your client may use a squat machine incorrectly, causing the barbell to fall on them. The client may then make a compensation claim against you since the injury occurred when they were under your supervision.

In this case, without public liability insurance, you would be liable to pay out the cost of the claim.

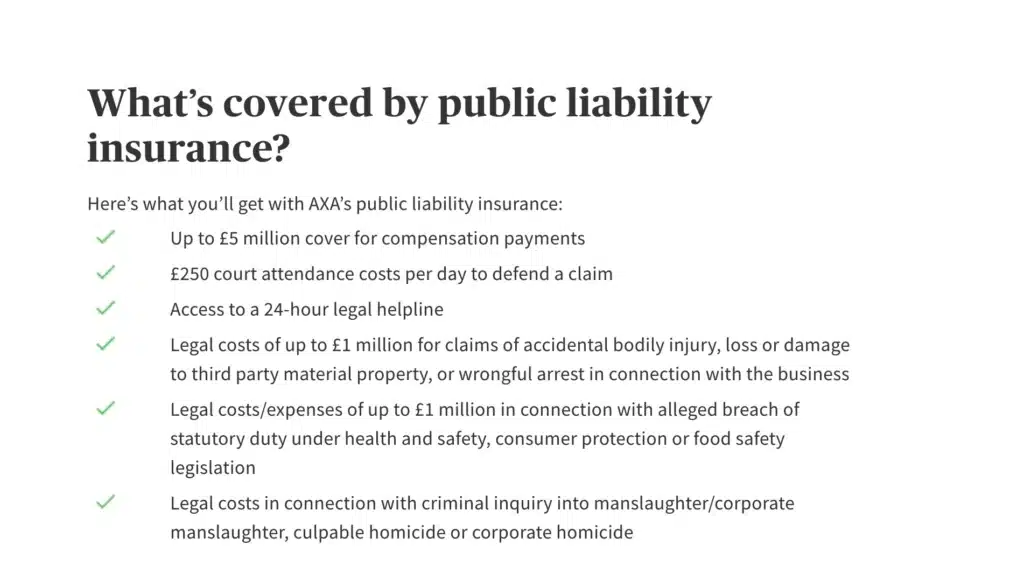

What is covered in AXA’s personal trainer public liability insurance gives a good indication of the types of things you can expect to be covered:

As accidents and injuries are common in personal training, you should also consider first aid for personal trainers so you know exactly what to do if clients are injured.

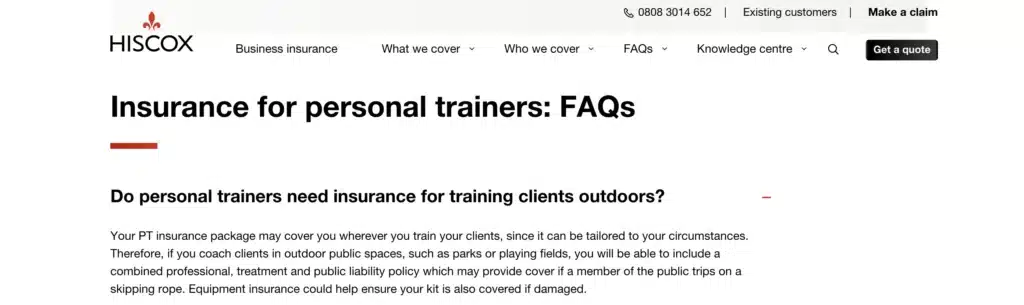

#2 – Personal Trainer Professional Indemnity Insurance

The next type of insurance you will legally need is personal trainer professional indemnity insurance.

This covers you if a client feels you have given them incorrect or bad advice which has caused them injury or illness.

Examples of claims a client could make against you are:

- Incorrect guidance on how to do an exercise

- A client doesn’t achieve their goals based on advice you have given them

- Inaccurate nutritional advice that has lead to illness or health problems

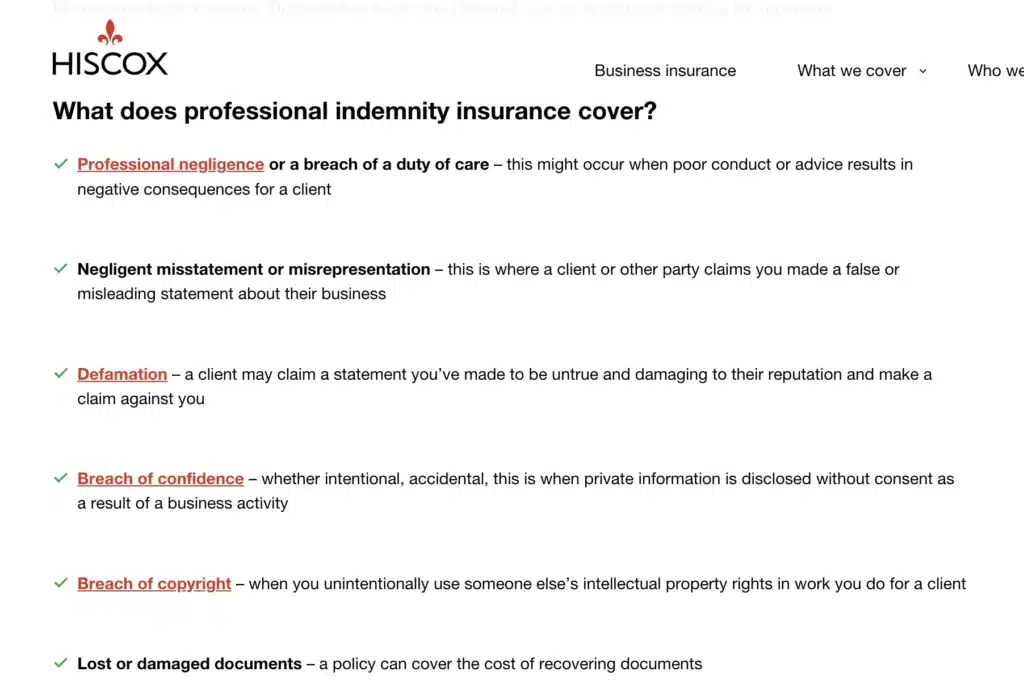

Hiscox’s provides an example of things a professional indemnity policy covers you for:

Recommended Additional Personal Training Insurance

There are some other types of insurance we strongly recommend getting. While not required by law, these include:

#1 – Personal Accident Insurance for Personal Trainers

This insurance for personal trainers covers you if you are injured or ill while working. Covering the cost of fees like injury treatment and rehabilitation, both short and long-term.

If you have personal accident insurance, most policies will cover the cost of your physiotherapy. It can also cover things such as medication, or short-term injury treatments such as operations.

The amount that you are covered for will vary from company to company, and depend on your policy.

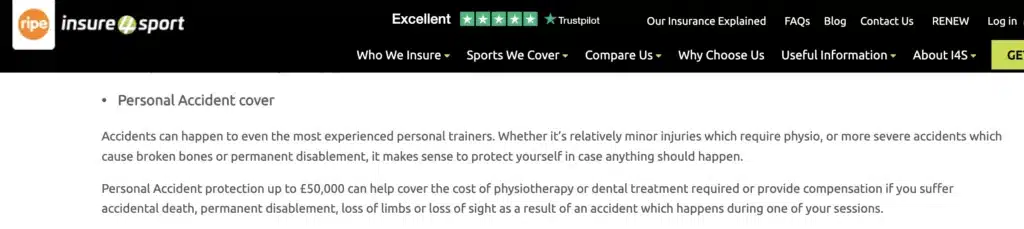

For example, Insure4Sport’s personal accident insurance for personal trainers policy says that it covers up to £50,000 for the cost of treatment and rehabilitation:

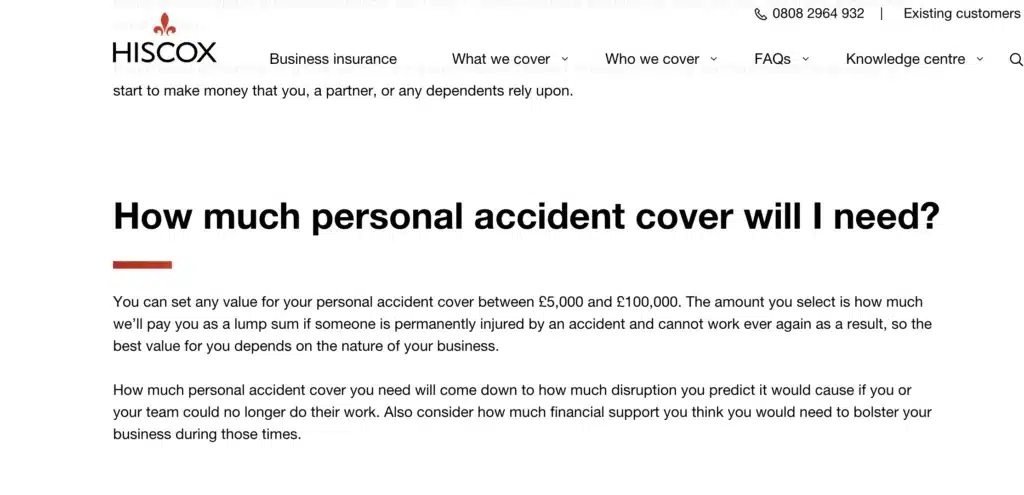

Whereas Hiscox says that you can set a value for your personal accident cover, between £5-100,000:

#2 – Loss of Earnings Insurance for Personal Trainers

If you’re injured while working as a PT, you may have no choice but to stop working while you recover. If you have a loss of earnings insurance, you will be covered in this kind of situation.

Where personal accident insurance covers the cost of your injury treatment and rehabilitation, loss of earnings insurance covers your expenses until you are well enough to start working again.

For example, Insure4Sport offers loss of earnings insurance for up to 52 weeks of you being out of work:

This is also why it’s important to have a PT cancellation policy as this also covers the cost when clients cancel on you.

#3 – Equipment Insurance for Personal Trainers

Equipment insurance for personal trainers covers you in the case of your equipment being lost, stolen or damaged. This can range from weights and exercise mats, to your professional laptop.

This type of personal trainer insurance is particularly useful if you are:

- A mobile personal trainer and take your own equipment to clients’ homes

- You run a PT bootcamp or fitness classes outside

- Own a gym or other space

The terms of personal trainer equipment insurance will vary between providers.

For example, Insure4Sport’s personal trainer insurance for equipment states that they will replace equipment if it is less than a year old with a maximum value of £2,500 per item:

Insurance for Working With Special Populations

If you’re a personal trainer for clients that fall under the category of ‘special populations’, you should make sure your personal trainer insurance policy covers you.

Some examples of special populations are:

- Disabled clients

- Elderly clients

- Pregnant clients

- Clients with health conditions such as diabetes

- Overweight clients

- Children

For example, if you want to become a personal trainer for kids, Insure4Sport states that they can cover you for working with children. But this might not be the case for other providers.

It is also important to note that many insurance companies will see working with special populations as a higher risk so may charge more for a policy to cover them.

– – – –

If you’re looking to expand your career skills in the fitness industry, these articles will help:

- Personal Trainer Resources

- Personal Trainer Marketing Strategies and Tips

- Starting A Personal Training Business Checklist (UK)

What Does Personal Trainer Insurance Cover?

Personal trainer insurance typically covers client injury claims, professional advice errors, personal injury, employee claims, and equipment damage.

Injury or Illness to Your Clients

Personal trainer insurance protects you if a client makes a claim against you.

This could be a claim of:

- Injury

- Illness

- Harassment

- Professional negligence

Having personal training insurance will protect you from having to pay this compensation if it happens during a session.

Injury or Illness to You

Personal trainer insurance can also protect you in the event of personal injury or illness. It will cover you financially if you’re unable to work or pay for treatment or healthcare.

Your Employees

If you have your own personal training business and employ staff, having business insurance will cover you if individuals are injured or fall ill while working for you.

Your Equipment & Property

Personal trainer insurance can also cover your equipment. This is in the case of damage, theft and loss. It can also extend to cover any property you own as part of your PT business, such as a studio or gym.

Do You Need Insurance As An Online Personal Trainer?

Yes, online personal trainers still need insurance, but you must ensure your policy covers remote coaching.

Some insurance providers don’t include online personal training as they have less control over clients than during face-to-face sessions. For example, you cannot physically correct a client’s form or provide support if an injury occurs.

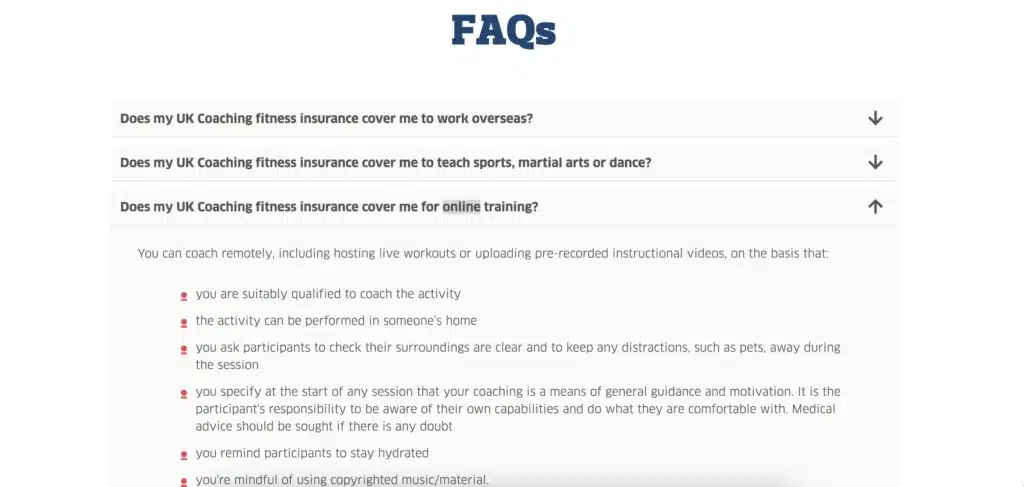

As online coaching has become more popular, many insurers now include online training within their policies, such as UK Coaching:

However, these policies often include specific terms and conditions that must be followed to remain covered. For example, you must stress that clients are aware of their own capabilities and limitations:

You can usually find this information on the insurer’s website or within the policy terms & conditions.

Do You Need Insurance If You Work in a Gym?

You may assume that working for a gym means you are automatically covered by their insurance policy, but this isn’t always the case.

Check with your employer whether insurance is included in your contract and what it covers. In many gyms, personal trainers are hired on a freelance basis, meaning you’re responsible for arranging your own insurance.

It’s also important to note that if you train clients outside of the gym, you may not be covered under the gym’s policy for incidents that happen away from their premises.

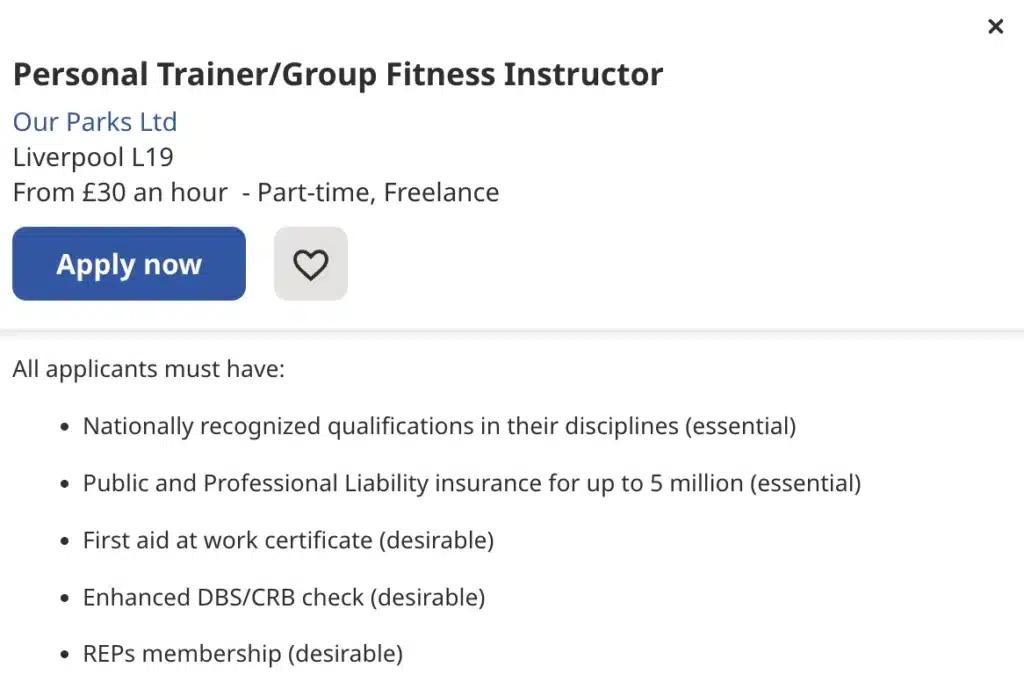

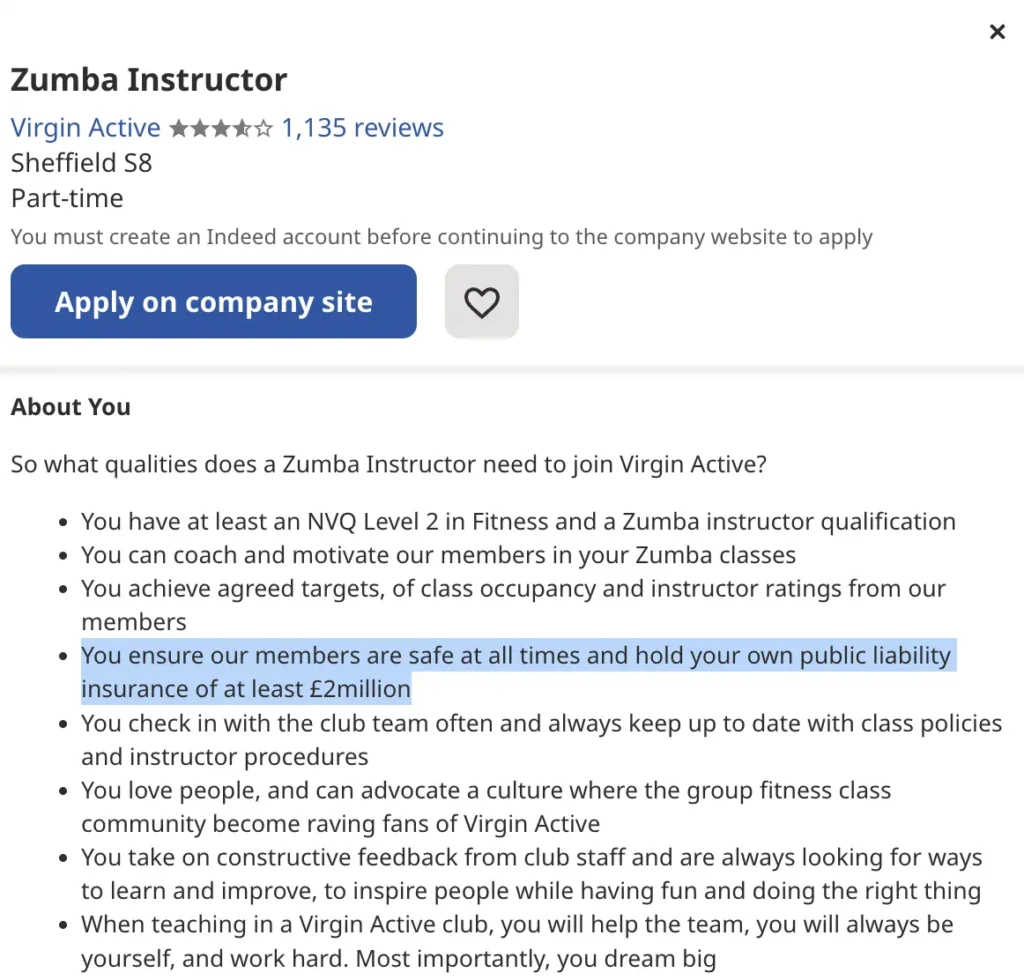

This is why many gyms state freelance personal trainers and group fitness instructors must have their own insurance, as shown in the job adverts below, which clearly states applicants need public liability and professional indemnity coverage:

Do You Need Insurance to Teach Group Fitness Classes?

If you become a group fitness instructor or teach group sessions as a PT, you will still need insurance coverage.

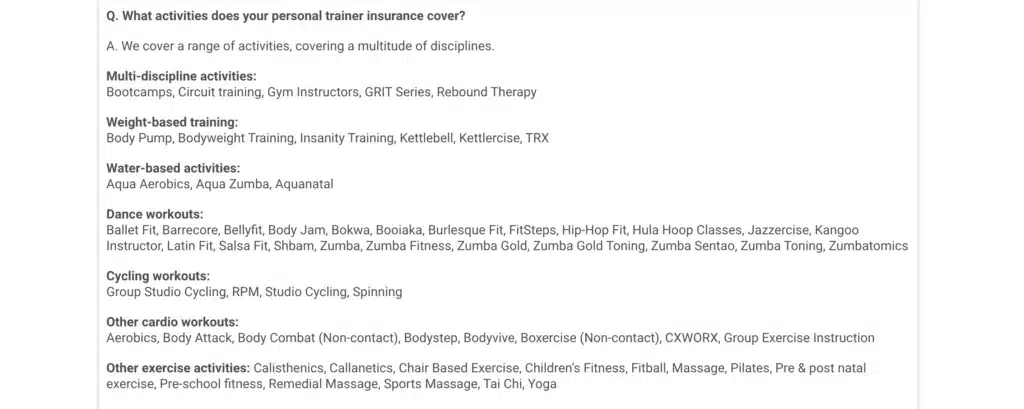

Most personal trainer insurance policies cover mainstream classes such as Zumba, Spin, and Les Mills. However, you should always check if your specific class is included in a policy.

For example, Protectivity lists the activities covered under its policy in the FAQ section of its website:

Many gyms also require group fitness instructors to have their own insurance before teaching classes, as shown in the job advert below:

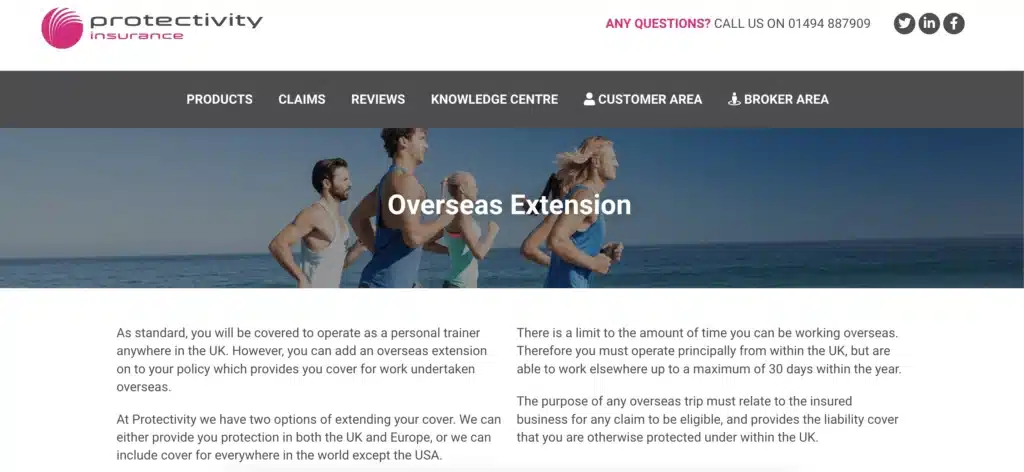

Do You Need Personal Trainer Insurance to Work Abroad?

If you plan to work as a personal trainer abroad, you should check your insurance policy includes overseas cover.

Most UK personal trainer insurance policies only cover trainers who work and reside in the UK.

For example, Insure4Sport’s personal trainer insurance policy states it doesn’t cover non UK residents:

However, some providers offer additional cover for trainers working abroad, which can often be added to an existing policy:

Do Personal Trainers Need Employer’s Liability Insurance?

If you employ staff as part of your PT business, you are legally required to have employer’s liability insurance. This covers claims made by employees for injuries or illnesses that occur while working for you.

However, most personal trainers operate as sole traders and work alone. If you do not employ anyone, you usually will not need employer’s liability insurance.

Most policies cover full-time staff, part-time staff, temporary workers, apprentices, volunteers, contractors, and ex-employees.

For example, if an employee injures themselves at your gym or workplace and holds you responsible, employer’s liability insurance can help cover compensation and legal costs.

How Much Is Insurance For a PT?

Personal trainer insurance costs vary depending on the type of cover you need, how you operate your business, and your overall level of risk.

What Affects Personal Trainer Insurance Costs?

Several factors can influence how much you pay for personal trainer insurance, including:

The Nature Of Your PT Business

The type of clients you work with and where you train can affect your insurance costs. For example, personal trainers for older clients may need more expensive cover due to the increased risk of injury.

The types of clients you train will also affect how much you charge as a personal trainer so check out our full guide on this!

Your training environment can also impact pricing. If you train clients outdoors or in multiple locations, you may need additional cover compared to trainers who only work in a gym.

For example, this insurance company explains the type of cover needed for outdoor training:

Your Level Of Cover

Policies with higher cover limits or additional protection, such as equipment insurance or online coaching cover, will usually cost more than basic policies.

Policy Length And Payment Method

Most personal trainer insurance policies range between 6 and 24 months. Longer policies can sometimes reduce your monthly or overall costs.

What Can Increase Insurance Premiums?

There are certain factors that may increase the cost of your personal trainer insurance over time.

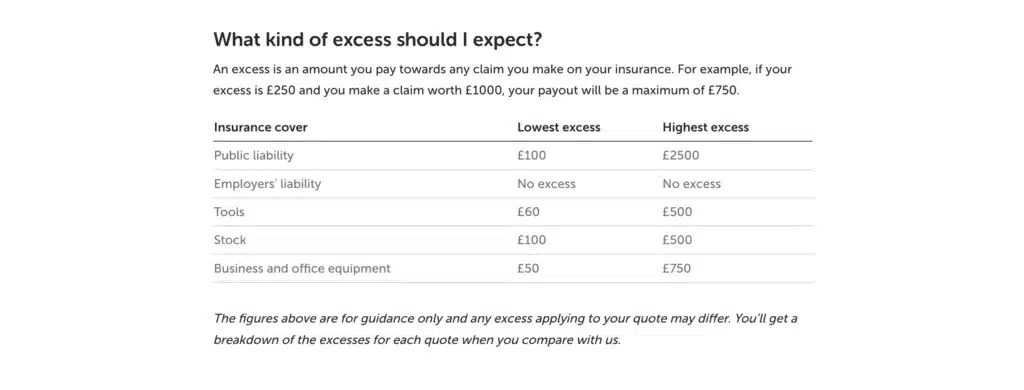

Claims History

Making a claim is one of the main reasons insurance premiums increase. Most insurers also charge an excess fee when you make a claim, although this is usually refunded if you are found not to be at fault.

This table from Simply Business shows examples of the excess fees included in some PT insurance policies:

Because of this, it is important to make sure you can afford the excess payment before submitting a claim.

Specialist Or Higher Risk Services

Insurance costs may also increase if your business involves specialist services or higher risk activities. For example, working with special populations or offering certain types of training may require additional cover.

How To Choose The Best Personal Training Insurance

The best personal trainer insurance in the UK depends on the type of cover you need, how you operate your business, and the level of protection included in the policy.

You should check:

- What activities and services are covered

- Whether online or outdoor training is included

- Public liability and professional indemnity limits

- Any exclusions or conditions in the policy

- The excess fee you would need to pay when making a claim

- Optional extras such as equipment cover or overseas protection

You should also make sure the policy suits the way you work. For example, a freelance PT working across multiple gyms may need different cover compared to an employed gym instructor.

Reviews can also help when choosing a provider, especially when checking customer service, claims handling, and overall reliability. It’s best to use impartial review platforms such as:

Keep in mind, a high rating based on thousands of reviews is usually more reliable than one based on only a small number of customers.

We’ve compared some of the main personal trainer insurance providers below:

| Company | Trustpilot Review Score | Number of Reviews |

|---|---|---|

| Insure4Sport | 4.7 | 5,372 |

| AXA | 4.1 | 20,080 |

| UK Coaching | 4.6 | 748 |

| Towergate Insurance | 3.4 | 1,836 |

| Hiscox | 4.7 | 562 |

| Markel | 4.0 | 251 |

| Protectivity | 4.8 | 868 |

| Simply Business | 4.2 | 7,274 |

Ultimately, the best personal trainer insurance is the policy that offers the right level of cover for your business, clients, and training environment.

Personal Trainer Insurance FAQs

What Insurance Do I Need as a Personal Trainer?

Most personal trainers need public liability insurance and professional indemnity insurance. Public liability insurance covers claims for injuries or property damage, while professional indemnity insurance protects you if a client claims your advice caused harm or injury.

Depending on how you work, you may also need additional cover for online coaching, outdoor training, equipment, or working abroad.

What is the Best Insurance for a Personal Trainer?

The best insurance for a personal trainer is a policy that includes public liability insurance, professional indemnity insurance, and cover for the way you work, such as online coaching, outdoor training, or freelance gym work.

When comparing policies, you should check the cover limits, included activities, policy exclusions, excess fees, and the provider’s customer reviews and claims support.

The best insurance provider will depend on your business setup, clients, and overall level of risk.

How Much is Insurance for a PT?

Personal trainer insurance costs vary depending on your level of cover, the type of clients you work with, and how you run your business.

Your insurance may cost more if you have made previous claims, work with higher risk populations, or offer specialist services such as outdoor or online training. Adding extra cover, such as equipment insurance, can also increase the price.

The best way to find affordable PT insurance is to compare quotes from different providers and choose a policy that matches your business needs and level of risk.

Do Online Personal Trainers Need Insurance?

Yes, online personal trainers still need insurance. Even when coaching remotely, clients could claim they were injured as a result of your advice or exercise instruction.

You should make sure your policy specifically covers online coaching, as not all personal trainer insurance policies include remote sessions as standard.

Before You Go!

Now you’ve learned about personal insurance requirements, there are plenty more personal trainer tips for beginners you should find out about!

Also, why not continue growing the services you offer with our Level 4 Sports Nutrition Course. Get in touch with our team to find out more or download our free course prospectus here.